Thomas Reports was created in 2006. For over 30 years Fred Thomas, III developed a successful career in real estate financing, focused on consumer lending. He is a licensed broker (DRE 01097630) and has managed over two-thousand closed transactions. ThomasReports was created to weave writings and passions under one platform; Real Estate, History, Travel & Culture, Politics and Technology. In today's social media demands, Thomas' voice has been recognized as an official Influencer, Tester and Reviewer for international marketing organizations.

Major League Baseball’s (MLB) preeminent event, the World Series just ended as the Texas Rangers achieved the 2023 crown. The typical road to winning the series is eleven victories but, in some instances, a wild card team will need another win. The Rangers triumphed over the Arizona Diamondbacks, who up until the word series were literally playing like “all world.” Unfortunately, the Rangers clipped off Arizona’s rattler and in dubious fashion got swept at home, and the final blow last night was being shut out. Congrats to all teams who earned the opportunity to play in the tournament.

Now that the games are over, some ask when will MLB come to its senses? I am an admitted baseball junkie and grew up on the premise that baseball is America’s pastime. But doesn’t the term World Series raise questions when in reality the tournament is comprised of MLB teams from the United States. Granted, MLB has done a great job in internationalizing the teams as of the over 700 players, there is representation from those from countries around the globe.

Who forgets the Wizard of Oz, when poor Toto inadvertently pulled the curtain off what was supposed to be Oz only to find a man standing behind the curtain? Thus, Oz’s reality of being a myth was uncovered.“

The World Series has become part of our culture. However, in fairness and keeping it real or being historically correct does the World Baseball Classic provide a better assessment of “World Champion?”

PHOENIX, ARIZONA – NOVEMBER 01: Corey Seager #5 of the Texas Rangers celebrates after the Texas Rangers beat the Arizona Diamondbacks 5-0 in Game Five to win the World Series at Chase Field on November 01, 2023 in Phoenix, Arizona. (Photo by Christian Petersen/Getty Images)MIAMI, FLORIDA – MARCH 21: Team Japan celebrates after defeating Team USA in the World Baseball Classic Championship at loanDepot park on March 21, 2023 in Miami, Florida. (Photo by Eric Espada/Getty Images)

Reaching classic car status (in production 25 years), as noted by Motor Trend Audi will retire its revolutionary “TT” sports car this year. Technically the car rolled out in Europe in 1998 but it was the 1999 model which came to the United States in 2000.

I was working on a short-term spacial photography gig in early 2000 and one of my assignments took me to San Francisco. It was there I noticed this trendy car zipping through the streets. My thought was ummmm?

As 2001 went by I remembered that look and occasionally, I would see another one. It was 2002 and my financial condition improved so I really started looking. At the time it was the basic coupe and the roadster. Finally, in March 2002 I found a pre-owned 2000 at a luxury dealer in Redondo Beach and it had limited mileage as well as having only one owner. I grabbed it and the rest is history. My office was in Pasadena and since it was still under warranty Rusnak Pasadena became my service dealer and they took care of all the issues you might have in wanting to bring your car back to perfection. However, there was an issue with one of the service advisors who felt more concerned about his advice versus accommodating my needs. I searched for a new dealer and even though Los Angeles Downtown Audi was closer to me, it seemed like a dealer not capable of meeting my needs I was wrong. You know what they say? First impressions can be everything! After making an appointment I was greeted by the tech who resembled a German and who wore a white smock. His name was Dennis and he assured me he would take care of my TT. Along with him and his Associate Valentin, who became my regular tech, they provided all the confidence I needed in assuring me the TT would be taken care of.

TT Runs

I joined a couple of Audi TT car clubs and met some great people as well as gaining knowledge of why these cars were so special. We would go on runs and other adventures and it was quite a site to see 50-75 TT’s rolling into various parts of the United States. Over the years I made modifications to my TT, although I must admit being somewhat intimidated to do so not wanting to void my warranty. Anyway, I added a chip to improve speed, wheels and other amenities. Perhaps the biggest mod that made my car stand out was adding a sunroof. When I was searching for the car, I could swear I saw the coupe with a sunroof. My eyes deceived me as the coupe did not have a TT. Even still, I had to have one. Despite being warned the roof would cave in as well as other calamities, I took the splurge and found an aftermarket installer located in Paramount, CA. I am 6’3” and the coupe is tight. The roadster is a no-go due to the way it is designed. It would be impossible to wedge my body into the car with the roof closed. However, the coupe was perfect as since it is part of the VW design and features lots of headroom, the sunroof was perfect.

The TT is a very fun car to drive. Looking back I am glad I realized in 2003 with miles stacking up, I needed purchase another “regular day” car so I opted for the A4, which itself had gone through a new design.

Sad to see it go….but

I am said to see the TT go. It was a revolutionary and the first sports car with an aerodynamic design. I liked the Porsche due chose not the chase the crowd because in my opinion, everybody has one. After Audi rolled out the TT, other manufacturers followed including Nissan, Honda, BMW and others who saw the benefit of the aerodynamic body. Plus, because the body offers a curved feature, which even today you will rarely see a model without it, the car was known as “ahead of its time.”

So, my TT is coming up on 24 years. It is in very good condition and yes, it is pampered. It has approximately 155,000 miles on it and even though I moved away from Valentin (due to cost of repairs at a dealer), I found Eurospec where Jeff and Peter provide the same confidence in making sure any repairs are legitimate but providing the care to make sure my investment is protected.

My current everyday car is a zippy A3 sedan.

At Red Rock in Las Vegas 110 MPH before topping off at 130MPH – NO TICKETAshland, ORUnder the hoodMontanaOld school Cocoa MatsOriginal look Durango, COCurrent look

Postscript – Audi is replacing the TT with another electric model to add to their growing lineup. That’s leaves the R8 as the only sports car in their stable.

Yesterday Major League Baseball started its annual playoff season. Perhaps coincidental, the nationally acclaimed documentary series – Frontline, presented a new piece “The Astros Edge” which focused on the cheating scandal in 2017. Bob Reiter did an excellent job in bringing you the details of the incident. Of course, some players as well as organizational staff did not participate in the interviews. One lad in particular was interesting. He was the staff responsible for setting up the TV in the locker room which aided the team as part of cheating. The Astros won the coveted World Series and while his salary was $45,000, the team granted him a cut of the series pool which in his case totaled $450,000.

LOS ANGELES, CA – NOVEMBER 01: Houston Astros owner and chairman Jim Crane hoists the Commissioner’s Trophy after the Astros defeated the Los Angeles Dodgers 5-1 in game seven to win the 2017 World Series at Dodger Stadium on November 1, 2017 in Los Angeles, California. (Photo by Kevork Djansezian/Getty Images)ORLANDO, FLORIDA – FEBRUARY 10: Major League Baseball Commissioner Rob Manfred walks to a press conference during an MLB owner’s meeting at the Waldorf Astoria on February 10, 2022 in Orlando, Florida. Manfred addressed the ongoing lockout of players, which owners put in place after the league’s collective bargaining agreement ended on December 1, 2021. (Photo by Julio Aguilar/Getty Images)

It took a couple of years to document the cheating but the ire to many is the decision made by MLB Commissioner Rob Manfred regarding the punishment rendered. While there were some who were terminated, suspended and/or fined Manfred apparently was snakebitten in the decision he made in allowing the Astros to maintain the crown of being the winner of the series. Instead of being true to the integrity he preached, he took the cowardly, if not political decision to claim, “no harm-no-foul.” despite the evidence being right in his face. What????? If you’re found guilty of something, like cheating how can you be rewarded by keeping the title you allegedly won?

Most agree, a more fair decision would have been to simply strip the Astros of the title and proclaim there was no winner for the year 2017. Manfred could not pull himself to do this and the rest is history.

a bird wouldn’t get caught if they didn’t open their mouth!”

We all understand the need to talk but some folk simply talk too much or talk themselves into trouble!

Today Donald Trump faced the music in front of Judge Engoron who last week found him guilty of fraud. Seated in the prosecution’s section and on the first row was one of Trump’s nemeses who has become a thorn in his butt, State Attorney Leticia James.

Most people who have basic common sense have known for too long that Trump is a master hustler or as the judge recently ruled a fraudster. His bluster is laughable, yet it gives pause because so many fall for it, including forking over to him their hard-earned cash. For years, he has crafted a persona of being uber-wealthy and one of the most successful businesspeople of all time. Many who knew better or should have known better couldn’t help themselves into believing Trump was all who he stated he was. Even the skeptics in this group have been caught in the buzz ever since he zipped down to escalator and announced his run for presidency. They feverishly wanted to believe everything Trump said despite the warnings that were right in their face. I only hire the best! I can wrap this deal up in minutes! I will show you how to put together a successful operation! On and on. Many figured….umm, why not, let’s give the lad some breathing room and see what he can deliver! After all, he looks the part.

Of all the bonehead mistakes Trump has brought on himself, one will go down as historic: turning against his former attorney and fixer Michael Cohen. It seems like years ago, as during his presidency Trump knew he was untouchable. He was the king, and nobody dared cross him. That is why the 2020 presidential election was so important. Those with common sense, knew if he did not have the presidency to shield him from all his illegal activity, understood the years 2021, 2022, 2023 and beyond would result in payback or the law catching up with him. So, as of this article he has historically achieved 91 charges and a host of other legal pitfalls.

Once Trump convinced Bill Barr to be his pseudo attorney and go after Michael Cohen, that may go down as the beginning to the end. Indeed, Barr through his role as the head justice official of the United States brought charges against Cohen resulting in his incarceration. Many in Trump’s orbit paid very little credibility to one of Cohen’s last acts as a public citizen on his way to the brig. On February 27, 2019 Former Congressman Elijah Cummings, who has sense passed, held a hearing where Cohen communicated to the House of Representative’s – House Oversight Committee Trump’s fraudulent behavior. Many knew of his behavior, but this was the first time a senior official in Trump’s organization gave up the gig and spilled the beans, in detail.

It was that hearing where some thought folk were sleeping, but Leticia James was taking copious notes. Her result was the ensuing charges and eventual guilty plea announced by Judge Engoron. Who knows what will happen to Donald Trump? Some, assume his basic strategy is to keep running for political office so he can continue to grift from those who support him as well as use his position as an excuse preventing actions against him because he is a viable candidate. More to follow……stay tuned.

“Our feets is tired but our souls [are] rested” Mother Pollard, renowned Civil Rights activist

Those who know us (Judith and me) understand our philosophy of trekking or touring spots of interest on a low or non-existent budget. Another difference in trekking is the sacrifice (lots of walking) required which is why many don’t dare venture into the experience. At the same time, many know about our trekks and are fascinated about the adventure – but as we warn BEWARE!!! Our friend Renie who is a foodie extraordinaire and who hails from Laurel has grown into a real tropper. For this journey, my sister Angela decided to give it a shot and we all had a great time.

We just successfully completed our EastcoastTrekk 2023, and the following recap is provided. This trek is important to us because we culminate it paying homage to the 1963 March on Washington which includes participating in events to commemorate the event. For this trek we needed to stretch it out but due to budget restrictions we needed to employ some creative strategies.

Departing at LAX, we did the red eye to Baltimore. After getting a brief nap at the Aloft Hotel Renie picked us up so we could grab lunch. From there we headed to DC so we could drop off our larger luggage before heading to Union Station to catch Amtrak for Charleston, South Carolina. We did a daytrip and later in the evening we boarded Amtrak for New York. It was also a day trip and later we boarded the Amtrak Acela for DC where we spent several days with March on Washington activities. Renie picked us up the last day which was Tuesday, August 29th, and we headed back to Baltimore, while also making a lunchbreak at world famous Pappas Crab Cakes.

I use an Epson pedometer watch which does a great job in documenting steps/miles, etc. Based on the data from the watch for this trek we did 56.2 miles!!!!

FIRST STOP – CHARLESTON, SOUTH CAROLINA

The International African American Museum (IAAM) was supposed to open January 2023. Our group was all set to be part of the inaugural visitors. Unfortunately, the venue was dealing with some issues and the opening was postponed. After some consideration we decided to wrap our visitation during our EastcoastTrekk which is always the end of August. In addition to visiting the museum we took time to visit the historic Mother Emmanuel AME church as well as our friend local Charlestonian, Joe Brown.

Today marks the 58th commemoration of the Watts Riots. Trivia buffs know this, but most do not:

The Riots did not start in Watts

Los Angeles is a large city. It is split into many neighborhoods and communities. For some, even African Americans think “Watts” is anything south of the I-10 (Santa Monica freeway).

In reality or being technical, Watts is a relatively small enclave of Los Angeles. The South border is Imperial Highway. The North border is Firestone Blvd. The East border is Alameda Street. The West border is Central Avenue

So, if the Riots did not start in Watts where did they start or what caused the spark?

The Riots started from an altercation with the California Highway Patrol and the Marquette Frye family. The location was an apartment complex on the west side of Avalon Blvd. near 115th Street. Technically that area is considered South Los Angeles or today South-Central Los Angeles.

Approximately two miles northeast, Watts had a primary business district on 103rd Street which became a hot spot as members of the community set it ablaze. Hence the name, “The Watts Riots”

Aerial view (drone) of the iconic Watts Towers which is the namesake of the community located on 108th & Santa Fe. Video courtesy of collection of Fred Thomas, III

In a democracy power is important. As George H. Bush exited the stage in 2008 people were ready for a change. To their surprise a young Senator named Barack Obama secured the presidency. He was young, promised change and yes, was African American. His supporters were ecstatic and even some staunch republicans figured how bad could it be? After all the economy was in a historic downfall.

Obama’s presidency broke traditional norms, especially from those who felt a certain way of how the country should be governed. Once he got settled in, those whose norms were turned upside-down or who had a different ideology caught their breath and went to work, all in a strategic effort to disrupt and marginalize his presidency.

Donald Trump, known as a master conspiracy theorist, came on the scene and went to work. He provided great appeal to those who were skeptical about Obama. The GOP scored big in the 2010 primary and were licking their chops knowing Obama’s days were numbered as the 2012 presidential election loomed. To their chagrin Obama pulled the hat trick and was reelected. The writing was on the wall, even though many dismissed basic facts. The GOP’s hardline stance on cultural issues, race and other factors were like an albatross around their neck as it related to national political races.

Trump’s popularity picked up steam and in 2015 he bludgeoned traditional GOP presidential candidates while securing the party’s nomination for the 2016 election. Over the years, many came to accept Trump’s antics, although some simply defined his behavior as savvy or shrewd. His bluster took center stage as his gift for gab became a rallying cry and the party felt they had finally found someone who could rebuild the GOP. Considered a master salesman, Trump knew which buttons to push and what to say to convince those in the party to give him the keys to the White House. He got the keys and quickly went into three-card monte mode. He promised Supreme Court judges, tax cuts and a few policies which were critically important to the party. In exchange he received permission to operate in a manner never seen by a United State president. Some call it grif or patronage or simply ripping off the public. He maintained a very charismatic posture and even those who you would have thought knew better realized it was too late as they were spellbound by the cultist support, he had created. From their desperation from allowing Obama to gain two terms, they created the Trump effect to take over the party. It comes to no surprise that many warned the GOP of Trump’s criminal behavior tendencies. Unfortunately, many chose to look the other way, while some were quite vocal that his administration operated akin to a mob family.

NEW YORK, NY – APRIL 04: Opponents of former President Donald Trump gather outside of the Manhattan Criminal Court during his arraignment on April 04, 2023 in New York City. Trump will be arraigned during his first court appearance today following an indictment by a grand jury that heard evidence about money paid to adult film star Stormy Daniels before the 2016 presidential election. With the indictment, Trump becomes the first former U.S. president in history to be charged with a criminal offense. (Photo by Spencer Platt/Getty Images)

So, while the GOP appears to be stuck with their choice in allowing Donald Trump to be their leader, his behavior in being shackled with indictment after indictment gives many in the party the Rip Van Winkle effect: What in the hell happened to our party? In 2018 he lost control of the House. In 2020 he lost control of the Senate and the Presidency. His legal box score has been historic. He has two impeachments under his belt. With the latest indictment on Tuesday for his efforts to try and stay in power, that makes three or it is four indictments he is facing. And that does not include the Georgia indictment which should be handed down any day. All this while he and his supporters claim he had done nothing wrong, let alone simply communicate free speech. Regardless of your party affiliation one simply must ask why one person gets caught up in so much legal turmoil? Is it truly a witch-hunt? And, if so, why are his so-called enemies out to get him? Is he that charismatic and his positives outweigh his negatives? All interesting questions but a professor once reminded their students of a simple adage, “A hundred Frenchman can’t be wrong!”

[postscript] Donald Trump was arraigned today at the Federal Courthouse in Washington, DC. As anticipated he pled 'NOT GUILTY" to the charges presented by special counsel Jack Smith. Trump's attorney's and his supporters claim the case boils down to FREE SPEECH which they claim he is entitled. Jack Smith and the prosecution see it a bit different as while they acknowledge Trump has free-speech authorities, the crimes they are alleging is his conduct and direction to criminally violate the laws. Interestingly the next hearing is on the same day as the 60th anniversary of the iconic March on Washington, August 28, 2023.

Preface – Since 2016 I have been working on my memoir. I pulled out the passage about my relationship with Countrywide, IndyMac Bank and Bank of America as well as personal knowledge of Angelo Mozilo to publish it here. My tenure at Bank of America closed June 2017 and I was officially headed towards retirement. No longer being shackled as an employee and risking any conflicts of interest I mapped out a timeline strategy to communicate my perspective. To get things going In February 2018 I reached out to my former IndyMac executive Mark Mozilo letting him know my plans as well as requesting his permission to use my anecdotal experience with his dad, Angelo. Mark agreed and offered his support.

Long Read

[West Adams] It was this past Monday that I was informed Angelo Mozilo had passed away the previous day. For some he was a visionary, a unique leader, a trailblazer. For others, he was the number one villain for the mortgage collapse of 2008. He was greedy and a manipulator as well as the prime culprit for putting borrowers in mortgages they could not afford, while racking in millions for himself and the companies he operated. No doubt, everyone is entitled to their own opinion. As for me, I have a more positive perspective.

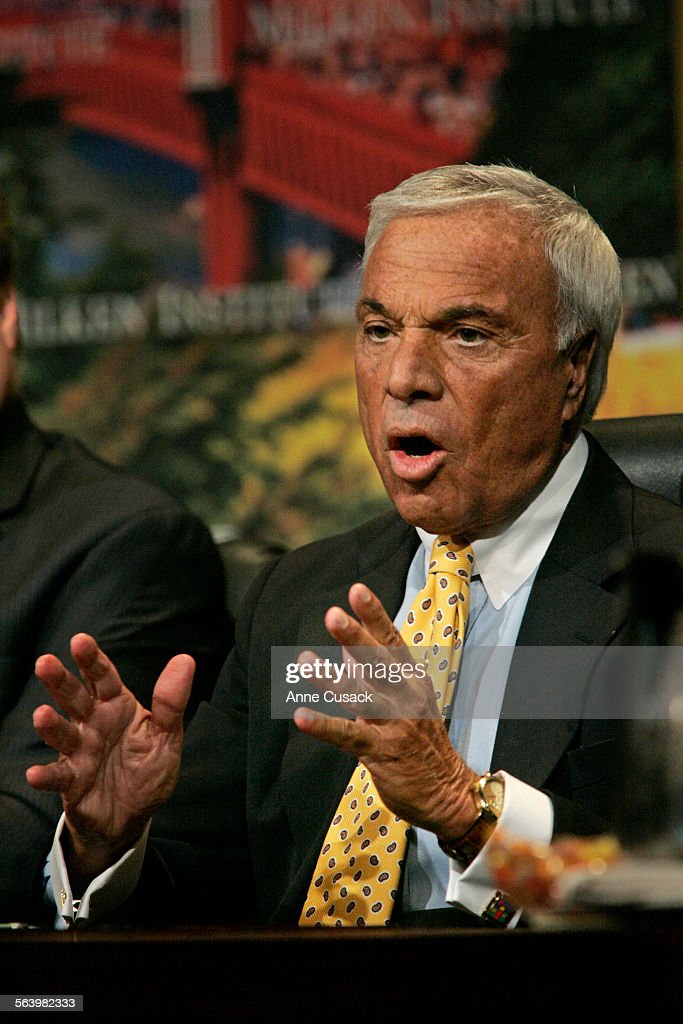

10/29/2007. Beverly Hills. Angelo Mozilo, Chairman and CEO, Countrywide Financial Corp. A panel discussion entitled Subprime Market Ripple Effect was held by the Milken Institute during the State of the State Conference held at the Beverly Hilton. The panelists L to R are Ross DeVol (CQ), Director, Regional Economics, Milken Institute; Bill Lockyer, Treasurer, State of California; Jeffrey Mezger (CQ), President, CEO and Director of the Board, KB Home; and Angelo Mozilo (CQ), Chairman and CEO, Countrywide Financial Corporation. (Photo by Anne Cusack/Los Angeles Times via Getty Images)

The Beginning

Home ownership was something I took for granted while growing up. It was basic shelter as the process, the financial obligation or generational wealth possibilities were never discussed. As a youngster I always had an interest in business. As an adult my formal education at the university level was marketing. In 1983 we bought our first property, and I was green as the grass outside. The process seemed to take forever and the person helping us with the loan came highly recommended but looking back the service he supplied was pathetic. Yes, we became homeowners but knew nothing about the experience we endured.

In early 1985 my role as a permanent staffer with the Los Angeles Olympic Organizing Committee ended[i] and like many we contemplated our next career move. The HR transition team offered the opportunity to look at those companies who were sponsors. American Express caught my attention. They had a subsidiary called Shearson Lehman and were developing their mortgage unit. I didn’t recognize it at the time, but several other large financial services companies were also jumping into the mortgage market. In addition to American Express, firms like Merrill Lynch, Metropolitan Life Insurance and others were setting up shop. They had a large consumer base, and the strategy was to leverage it with products offered by subsidiaries they created. This was all to create a one-stop shop.

I went through the interview process and became a mortgage banker, a person who sells mortgages to consumers, using relationships with decision makers such as realtors, attorney’s, accountant’s and other professionals. For me, it was an eye-opening experience, and I was on a very quick learning curve.

Even in those days lending was pretty basic. Borrowers preferred a fixed rate loan but at the time rates were in the high teens. Whereas, the one-year adjustable-rate mortgage at 10% that Shearson was offering looked pretty attractive. As part of my marketing efforts, I was active with the Board of Realtors. I recall many top producers who would snicker at this company called Countrywide. In fact, one of the statements used to marginalize lenders or mortgage bankers like Countrywide, Shearson and the like was “we use our own money!” During my first year at Shearson, I would hear more experienced staff mention mortgage brokers. That word was forbidden and was like the kiss of death if ever mentioned. They were considered less than crooks, rip-off artists and the like. It was territory you did not want to venture into. That piqued my curiosity, and I started quietly trying to figure out exactly how they fit in the world of mortgage lending. I came to my senses and realized Shearson was not the fit I projected. While they were a financial powerhouse, their mortgage unit came about by buying a small lender headquartered in the inland empire. Their focus had been traditional conventional mortgages as well government sponsored mortgages (FHA/VA). They were not equipped to handle high-wealth borrowers where underwriting required a higher level of knowledge and sophistication in comprehending their financial documents. My clientele was West Los Angeles including exclusive areas such as Beverly Hills, Brentwood, Hollywood Hills, etc. Even though I was producing loans from this area, just about each one ran into issues.

“Had I known what I eventually came to know I would have selected a more aggressive lender. In doing so, I often quip, I would be rich from the fees I would have earned. Instead I became “broke as a bell glade Indian. It was embarrassing to engage wealthy clients who earned more money in a month than I was making all year, only to tell them they didn’t meet underwriting guidelines.”

Mortgage Brokerage

I rolled the dice and made a quiet exit to explore the myths of mortgage brokerage. I found a new home with a small shop in Torrance. Their production had stalled and needed someone to manage their sales team. It was a short-lived experience, but I learned quite a bit. The owner was eager to turn the company around. I’m a pretty conservative business-oriented person, some might label me as lame! The owner was of Japanese-Hawaiian descent, a nice person. Back in those days marijuana was not legal. He had a penchant as we would go and visit clients to roll-up a blunt and smoke away. It’s laughable when I think about it. I left and in early 1987 felt the time was right to set up my own shop.

Of all the things I learned about how to run a brokerage I was intrigued by how revenue was collected. As a broker you received payment as soon as the loan recorded. Whereas, as an employee such as when I was with Shearson you were paid at the end of the month. This was critical because once I knew legitimate mortgage brokers could get approved, the next hurdle was making sure we had solid points of contacts should any issue arise

Also, during the Shearson days, Countrywide was quietly starting to grow. A recruiter reached out to me to interview for one of the branch manager positions. My heart was set to learn the role of mortgage brokerage, but the experience helped broaden my perspective in lending.

Another noticeable reality was consumer attitudes towards mortgage brokers were shifting. Once I understood the role, how they operated, how they created revenue my thought was “how hard could this be?” My strategy was simple and driven by the service paradigm. Be available and offer clients better service than competitors.

During that time lenders got wind of how brokers were affecting their market and started creating wholesale divisions. Countrywide was no different as they too started courting mortgage broker business.

Countrywide was still considered “not a big-league lender” at least that is what I was hearing at the weekly Board of Realtor meetings. Then something happened! In 1988, there was a monetary crisis and the banks and savings and loans took the brunt of the beating. They were no longer a practical source of competitive mortgage loans. That left Countrywide standing tall as they didn’t require using borrower funds to make loans and out of the darkness they rose in popularity.

As I was setting up my list of lenders I focused on Countrywide. My office was downtown Los Angeles, and they were in Pasadena, so my feeling was any issues were just a quick drive north. This turned out to be a great decision.

Meeting Angelo

We started out as a fledgling company, severally undercapitalized but with big ideas and an aspirational vision on what we might become. Part of running any business is networking. There was a mortgage brokers workshop in Long Beach. If I’m not mistaken it was at the Marriott on Ocean Blvd. I had arranged to meet several prospective lenders and one of them was the executives at Countrywide. I was to meet the head of their wholesale division, Rick Cossano. Once I arrived at the hotel and made the rounds, I started looking around for him. Not knowing what he looked like I ran into a sharply dressed gentleman and asked was he Rick Cossano? He said, “no my name is Angelo Mozilo, but Rick is right over there,” so he took me over and connected us.

That is how it was back in the day as mortgage brokers were trying to get their footing and top executives would frequent these types of sessions. They were looking for consistent brokers to grow their wholesale business and brokers were looking for lenders who could help them grow their originations. As mentioned, in the late 80’s as traditional banks and savings and loan had to take a back seat, lenders like Countrywide changed Realtors and borrower’s attitudes about how mortgage bankers, through legitimate brokers could play a crucial role in providing competitive mortgages. The trick was to not disrupt or jeopardize their existing origination channels.

Angelo Mozilo was a visionary and empowered executives like Cossano to undergird small firms like ours to generate steady production. In the early 1990’s Countrywide’s business was taking off. They developed a national retail network backed by the strategy to brand themselves as the lender of choice. This was coincidental as they also built a solid servicing platform as with originations picked up for most lenders, many found themselves without the ability to service or accept the borrower’s monthly payments. This became a gold-mine for Countrywide as their servicing portfolio was growing leaps and bounds and became a critical marketing asset for them, especially when those customers wanted to refinance their existing mortgage or buy a new home.

In my opinion, another critical benchmark of the consumer mortgage business was Angelo’s leadership and voice to persuade the institutional investment community to change or grow with consumer behavior. Angelo understood the nexus. He took over as president of the Mortgage Bankers Association. Part of his advocacy would help the secondary lenders understand how to create lending programs to accommodate high-wealth clients as well as those with non-traditional income streams. The strategy paid off as production across the board soared to new heights.

Angelo Mozilo was always gracious with us. He implored his wholesale executives to supply whatever support they could legally supply to ensure we were successful. In fact, while attending mortgage broker conventions, it was not uncommon if he was going to be in attendance to direct his staff to allow Judith and I to join him at their table. Make no mistake, I appreciated the generosity but understood the gesture was more of an investment to make sure we consistently produced quality business for them.

1992

In 1992 riots blazed in Los Angeles. It spoke to the inequities some felt as well as the racial animus that created the attitude. Many companies and organizations scrambled to prove they were sensitive to all parts of the community. In the case of Countrywide, they were in somewhat of a pickle. Even though their name had grown as a top lender, the minority community had a different perspective. They felt companies like Countrywide only catered to well-heeled bedroom community clients and certainly offered no presence in their communities. As mentioned, our business was growing. We were housed in the FHA headquarters west of downtown Los Angeles, on the 10th floor. My office faced south, and you could see the smoke and blaze through the windows. I received a call from Countrywide as they needed a minority firm such as ours to offer support or confirm, they were trying to service the community. The publication was the Wall Street journal. From there our relationship grew stronger and stronger as we were able to document borrowers who were now homeowners from the mortgages we originated and sold to them.

The relationship with Countrywide opened many doors. To keep pace, we simply could not produce enough volume needed for the aspiration sought. I could not raise enough operating capital to keep pace. In the middle of 1995, I called our staff in my office and announced we simply were out of gas. That meant closing our doors. Most of the revenue we generated was used to grow our business. We still had personal obligations including raising our family as our oldest daughter was headed to college. In a financial pickle with no source of income I needed to secure employment immediately. Countrywide was our core institutional client, and they needed staff to grow their business. Rick Cossano arranged for Judith and I to be quick hires so we could accumulate paychecks to get back on our feet. It was a humbling experience to walk through the offices at 155 N. Lake. Instead of a high-flyer mortgage broker, I became just one of many thousands of employees.

Initially, I was placed at the 35 Lake building and our unit eventually moved to the main headquarters at 155 N. Lake. It was not uncommon to run into Angelo, although I kept a very low profile. He was a taskmaster who was impeccably dressed and commanded attention wherever he stepped. For many staff and this goes back to our days when we would see him at the mortgage broker conventions, staff was petrified of him. If something was out of place you could count on being admonished. In those days, as for men you had to have a nice supply of quality white shirts and sharp contrasting ties. Luckily for me, I never felt that intimidation, perhaps because we met at a different level. Even still, I always had the greatest respect.

Countrywide was booming. In late 1996 rumors were circulating that Bank of America was trying to buy them. I recall at the Lake headquarters, Angelo called an impromptu meeting in the lobby and the focus of his message was to calm staff, while letting them know the rumor had no validity. By 1997 there was an explosion. 155 N. Lake was simply too small to house the growing giant. Corporate was moved to the former Lockheed headquarters in Calabasas which offered a large campus. Other divisions also found new homes. My unit moved to what was known as “Title Row” based on the substantial number of Title Companies who moved to Rosemead. They had since left but Countrywide quickly filled up a prime spot. Another major relocation was in Plano, Texas as that campus also offered a sprawling campus.

Much has been written about Angelo Mozilo. As the mortgage industry collapsed in the mid 2000’s most of it has been negative and one sided. Some of it provides glee in authors blaming Mozilo for all the world’s ills.

As gifted as Angelo was, he was no magician. He had a vision of opening home ownership to the masses. Yes, this included creating programs were those who had been shut out, for once finally felt they had a chance at the “American Dream.”

Mozilo didn’t create sub-prime lending, or the 125% or any of the products traditionalist define as extreme. Markets change from time to time and there will always be a cadre of lenders offering products, however risky to provide an opportunity to borrowers. In Countrywide’s case it was a double-edged sword. They had built a service business, the envy of the industry. The borrowers were loyal to them but also had needs. As much loyalty they claimed, they understood if Countrywide didn’t offer the product or loan they were seeking, they would have no choice but to leave them. Countrywide and Mozilo knew this and recognized the value they had created in their portfolio so rather than bleed customers to those providing riskier mortgages, they felt they had no choice but to expand their borrower portfolio from “blue-chip” to various levels of creditworthiness and complement it with sub-prime products. Of course, it’s no secret the riskier the mortgage, the more fees or increased revenue is the result. If the treadmill was running smoothly, nobody was hurt and revenues more than justified the risk.

Mozilo tried to stead the ship. Their growth was phenomenal, but the crash eventually caught up with them. They got labeled as the Sub-prime factory of the world but that is not a fair assessment, as that market was just a small part of their overall production.

From the Hero to the Goat

When Countrywide launched in 1969, they quietly took their place as an upstart mortgage banker whose specialty was providing fixed rate mortgages. Over the years they simply outlasted their competition and built an impressive franchise buffered by their servicing division with loan originations coming from their retail and branch network, their correspondent division and their wholesale division whose production had skyrocketed to numbers similar to retail. All of this resulted in the team becoming the number one leader in America. They were the darling of the industry and Angelo’s Midas touch was being handsomely rewarded.

The arrival of the 12 MAT

In 1993, Angelo and the team started a warehouse division which was housed down the street from corporate headquarters called the 35 N. Lake building. They were responsible for bundling and selling the avalanche of mortgage production. This dubious division was called Countrywide Warehouse Company. They were considered an incubator. As Countrywide grew, they grew as well. Once Angelo moved corporate to Calabasas, Countrywide Warehouse moved to the 155 N. Lake building. It was the mid to late 90’s and the dot-com fever was sweeping the nation. Countrywide Warehouse had grown enough to ditch the Countrywide moniker, changing their name to IndyMac. Their focus was doing things outside the lines, taking a revolutionary mindset while creating the tag line, “Bureaucracy Beware.”

It was like the wild wild west. In 1998 I joined another Countrywide subsidiary headed by my friend Rick Cossano called Landsafe Title. I was housed back at the 35 N. Lake building and would visit the 155 N. Lake building to chat with friends or go to the credit union. What I saw was remarkable.

As mentioned, Angelo Mozilo had built Countrywide into a respected powerhouse. Staff were well-dressed and conducted themselves in a manner that would not create ire from Mozilo’s lieutenants or those who might see something unacceptable to the environment created. As mentioned, at Countrywide quality white shirts with nice looking contrasting ties was the norm for men. The upstart called IndyMac who no longer lived under the threat of reprisal from Countrywide had an opposite environment. Again, this was during the dot-com days when offices were being transformed to campuses. Staff worked hard and put in long hours. Their dress was more relaxed plus there were amenities offered to compensate for your time at the office. There were game rooms, lunch/dinner was often brought in and a complete array of services that was a new wave of how professionals operated in a business climate.

Instead of heavily starched white shirts I would see staff in nice-looking polo shirts and matching shorts. On Friday’s staff was treated to beer and other refreshments. On the business side they were building an impressive portfolio catering to mortgage brokers and correspondents. They did not have a typical retail origination channel. To note, there was also a shift in borrowers’ employment and how they received income. Underwriting guidelines had also changed, and risk-based pricing became the norm.

The idea was simple and based on credit scoring. The assumption was correlation between credit score and liquid assets used to support income.

They created a mortgage program which became a breadwinner for the secondary market. It was called the 12 MAT (Moving Treasury Average). The core feature was borrowers were afforded four payments, the least interest only. It was designed for borrowers who had good credit but whose income fluctuated or making it hard to document in a traditional manner, typically those self-employed. As an alternative borrowers could document income by the number of consistent deposits in their banking accounts. The program was not designed for traditional W-2 employees or whose income did not fluctuate. Issues started to arise as the 12MAT became popular and borrowers would boast about only being compelled to pay interest only or the minimum payment, while others were “stuck” with traditional fixed fully amortized payments. Who wouldn’t want to have the lowest payment option? The appetite for borrowers to get the mortgage was ferocious. It became misunderstood and took on a negative connotation as some originators, along with borrower cooperation caught on to guideline of stated income. In other words, if you somehow could document the amount from bank statements you could put whatever income was needed to qualify for the loan. It would later become defined as the “Liar Loan.” As the industry once again shifted in the mid 2000’s, home values stalled, and borrowers could not refinance those mortgages. The walls closed in and eventually the mortgage collapse occurred. Yes, the 12MAT program was the main culprit and yes companies made huge sums of money but there is more to the story than issuing blame.

The Dot-Com crash

In the late 90’s the dot-com era wiped out many dreams. IndyMac was left standing and labeled itself as one of few companies who survived that era. Rick Cossano departed Landsafe in 1999 and I along with several staff who had joined him from Countrywide saw the writing on the wall and eventually left later in the year. I learned later that Indy Mac had created the type of environment which appeared more creative than Countrywide. Long-time Countrywide staff was jumping ship and joining the growth train at IndyMac. Eventually Countrywide management had to place a moratorium and other guidelines on staff movement.

After leaving Countrywide I took a personal break and headed to Chiapas, Mexico and eventually got into spacial photography (think Google maps) and wound up in San Francisco. As I headed back to Los Angeles, I knew I had to buckle down and resume my mortgage career. B2B (Business to Business) was an acronym created from the dot-com era. It was brought to my attention IndyMac was growing a division catering to realtors and it was called Loanworks. I joined the firm and was stunned to see so many Countrywide colleagues. Corporate headquarters had moved from the 155 N. Lake building to a newly reformed campus in East Pasadena. The response I would hear from those colleagues who had left Countrywide was, “this is great, it’s just like Countrywide, just smaller and a nicer environment.”

Like Countrywide, IndyMac was flying high. The year was 2001 and 911 occurred later in the year. In In late 2002 Loanworks had a change in executive management and Mark Mozilo took over the helm. As mentioned, I first met him during the early days of our mortgage brokerage operation. He was also Angele’s eldest son. It was quite a site at IndyMac as even though Angelo was doing his thing in Calabasas, his two sons Mark and Eric, were at IndyMac. Mark and I would have chats how his dad was having fits of how IndyMac staff was dressed while operating a business. Mark would joke how he threatened him that his next move was to grow a beard!

Nothing last forever

In 2005 Mark took on a new assignment. IndyMac bank, which had only one physical location, was growing that division and I was plucked to run the group of loan officers needed to staff them. The reality of the market changing was communicated to be by one of my trainers, Jerry Timpone. A noted real estate guru he would come dashing in my office warning me a wave was headed our way. I shined him on but looking back I must admit how prophetic he was. You could see the writing on the wall that even though we had new branches which were handsomely appointed, production was tough to come by. In mid-2006 Indy Mac stock was at an all-time high. Our division closed. I left and luckily was able to cash in from my 5 years of hard work. Interestingly, as I was wrapping up my career at IndyMac, I received a call from a recruiter encouraging me to entertain a spot at Countrywide. I visited one of their offices at 2 S. Lake and listened to their pitch. It was simple. They had taken off and were on a quest to achieve 200,000 employees. It was appealing but my personality was not to repeat of go back to a company I had left. Judith and I took off for a short trip to Belize.

In 2007, the gig was up. Somehow IndyMac was targeted as the primary culprit of the real estate market crashing. There was a run on the bank deposits. Also, it didn’t help that New York Senator Chuck Schumer went on national television to foment how companies such as IndyMac was a threat to the national economy. Unfortunately, it became the first bank seized by regulators or the face of what was wrong with banking and the mortgage industry.

Bank of America finally got their treasured prize.

As the market continued to implode and a hefty percentage of borrowers could not keep regular payments one by one, they were forced to close. Countrywide was not left unscathed. There was news they needed a cash infusion to mitigate their ability to keep operations. As you might imagine over the years many suitors noticed Countrywide meteoric rise. From my discussions with Mark, Angelo was adamant about not selling as he took immense pride in building an independent company that was number one in the industry.

Bank of America would not take no for an answer. They too were growing, and it was no mistake they have their eyes on Countrywide’s efficient retail branch network as well as their coveted servicing division. A deal was cut. Angelo finally gave in; Bank of America would supply the needed cash and in return they would get the franchise they were licking their chops to obtain.

Implosions continued and foreclosures were spiking at historic rates. Many blamed the collapse on borrowers obtaining mortgages they didn’t understand or simply had too many risks. Of course, with IndyMac already receiving a black eye, it was not surprising to blame the ills of the industry on whoever was not there. In that case, it was Angelo Mozilo who had drifted into retirement after settling regulator’s lawsuits. Sadly, Bank of America tried to defend its purchase of Countrywide by saying they were duped by Mozilo. It was rarely mentioned they had been chasing Countrywide for years. They had bought an albatross which almost took them out as well. Through the years they continued to recover but had a recognizable foil in Mozilo and Countrywide. They would become the negative eyesore of any issues Bank of America would have to confront. With the purchase of Countrywide, Bank of America absorbed a large percentage of their staff. Many had started their tenue in the early 2000’s and they quietly took their place and had to accept the narrative that was communicated about Countrywide. It became quite a talking point as over the years employees had been transformed to speak negatively about Countrywide and their standards and work-ethic, or lack thereof, at least from their perspective. Perhaps they had forgotten the positive things they experienced at Countrywide? Many lacked the depth or perspective of mortgage lending or didn’t care about history, as for them it was simply just a job. Industry-wise, Bank America was not a player in the mortgage business which makes you wonder why the purchased Countrywide in the first place? Of course, as the story unfolded some will say they were forced into it. Their core business was banking but, in the end, they were able to merge what was left from Countrywide’s assets into their own. Nevertheless, it was still puzzling for me to hear from colleagues what I thought should have been a more honest assessment.

It was an unfortunate legacy that Angelo and his family had to live with. Countrywide and Bank of America were two separate organizations. Again, Countrywide built a reputation as a trailblazer while Bank of America was known as a “button-down” shirt type of company, taking extraordinarily negligible risk while growing its network through acquisitions.

No lie can live forever.

I always respected how Angelo Mozilo grew his company. Some of it, I saw first-hand. As outlined my perspectives are not based on something I read. Admittedly, to see the downfall of his beloved Countrywide was painful to see. In the early teens of 2000, my sights were set on winding down my career so I could head into retirement and tackle the many personal projects I had assembled. Bank of America had stabilized and ever since leaving IndyMac my focus in staying in the industry was to seek out opportunities to use my experience with different departments. Due to the real estate meltdown compliance groups were growing and I projected that would be a nice landing spot to fade out. I was contacted by one of my recruiter contacts informing me of a new opportunity at Bank of America at their Calabasas campus. I joined the newly formed team, and the rest is history. While the work and new discipline in Compliance was challenging, it was painful if not at times irritating when speaking to various colleagues. It seemed those at Bank of America were in a trance, let alone have any depth or understanding of the mortgage industry. Most bought lock, stock and barrel the notion that Angelo Mozilo was some type of villain and Countrywide was one of the worst-run companies on the planet. The attitude was like that of a cult. They didn’t want to hear how Angelo was a visionary. How he changed underwriting guidelines. How he supplied opportunities to homeowners like nobody before him, on and on. Whenever the name Countrywide would come up, all I would hear was how they almost took down Bank of America. There was never any mention of how it was Bank of America who was chasing Countrywide.

During my years at Bank of America, my writing was noticed, and I became a writer for several digital publications to focus on the mortgage industry. This was more of a side gig as I was committed to Bank of America during the day as a full-time staffer. One caveat I had to adhere to when publishing my articles would be not to mention Countrywide or Bank of America. In 2017 I was finally set free as I left Bank of America and no longer bound to keep quiet.

Like most of us, there are good parts and there are bad. The Angelo Mozilo I knew was a trailblazer. The positive things he did while living is noteworthy, and nobody can tarnish that reality. Yes, he was the co-founder of Countrywide and responsible for their record growth as well as their eventual demise but in the game of life you don’t have to bat 1000%

RIP Angelo Mozilo – unlike some, you at least tried.

The Leaguewas released yesterday, and it is a must-watch. You don’t have to be a historian, a baseball nerd, a fan of The Negro Leagues or just an uninterested person to appreciate what this documentary presents.

The doc chronicles the life of the Negro League. From its glorious successful rise to its unfortunate demise. The lore is unmistakable as it became a seminal part of American culture.

Photo courtesy of the Fred Thomas, III Collection. The playing field as seen in the Negro League Museum – Kansas City, MO

Against all odds the Negro Leagues built an organization that debunked the notion African Americans were less than. It caught the eyes of the most critical naysayers and became the model in how baseball would be transformed. As the Negro Leagues were ascending in popularity the “White” game known as Major League Baseball (MLB) was floundering. The game lacked the energy fans were reading in newspapers about how exciting the Negro Leagues games were performed.

No doubt, Branch Rickey deserves credit for taking the lead and bringing Jackie Robinson into MLB. Indeed, but he was no saint or some social revolutionary! As a matter of fact, MLB had warned him and others who knew the benefits of players from the Negro Leagues to not mess with the Jim Crow standards the country had adopted. It’s a good thing he was a bit hard-headed as for him, it was about making money. As great a feat that moment was, it marked the eventually downfall of the Negro League.

The death knell

Back in those days there was no free-agency and owners literally owned players. In the Negro League there were gentlemen’s agreements regarding player movement and buying contracts. Owners were often outbid as well as other shenanigans that took place, all in the effort to field the best team that would yield financial success. The doc shines as it chronicles a critical part of history that is rarely, if ever spoken.

Former Chicago American Giants player/manager Dave Malarcher asked Newark Eagles co-owner Effa Manely when did integration happen,? “When the major leagues saw those 50,000 Negroes in the ball park at the East-West game, Branch Rickey had something else on his mind other than a little black boy. He had those crowds.”

In 1949 Tom Baird, still bitter about not being compensated for Robinson wrote, “I have been informed that Mr Rickey is a very religious man. If such is true, it appears his religion runs toward the almighty dollar.”

Once the Dodgers signed Jackie Robinson and the floodgates opened for other players in the Negro League, there was an all-out assault for the other MLB teams to join and grab top talent from well-known teams. The problem was, as players were brought into MLB, the teams they left rarely received fair compensation for all of the investment they made to create value in them. As you can imagine, as top talent departed the energy of the league declined. Further the millions of African American fans who flooded the stadiums to support the League turned their financial resources to MLB teams to see how the Black players were performing. The rest is history.

The doc shows the ruth fullness of Branch Rickey and those like him who marginalized the Negro League owners while downplaying their significance, as if the stars were born out of the sky!!!!! They raided the league during the late 40’s to the late 50’s until their eventual death in the early 60’s. Imagine if you had a business and created and developed talent, only to find another party grab your most critical assets while compensating you pennies on the dollars?

WATCH THE DOC!!!!!!

The doc can be seen on Amazon Prime, Apple TV and most popular streaming services.