Above caption. Federal Reserve Chairman Jerome Powell Holds A News Conference Following Federal Open Market Committee Meeting

WASHINGTON, DC - SEPTEMBER 26: Federal Reserve Board Chairman Jerome Powell speaks during a news conference on September 26, 2018 in Washington, DC. The US Federal Reserve raised the short-term interest rates by a quarter percentage point on Wednesday, the third increase of the year, and signaled two more hikes were coming in 2018 and four in 2019. (Photo by Mark Wilson/Getty Images)

CHICAGO, IL – SEPTEMBER 26: Traders monitor offers in the S&P options pit at the Cboe Global Markets exchange shortly after the Federal Reserve announced it was raising interest rates on September 26, 2018 in Chicago, Illinois. The Fed agreed to increase the federal funds rate a quarter percentage point, to a range of 2% to 2.25%. (Photo by Scott Olson/Getty Images)

[Washington, DC] In a move that was forecast several weeks ago, this afternoon Jerome Powell, chairman of the Federal Reserve raised the discount rate to 2.250%. This move occurred to the chagrin of his boss and the person who appointed him Donald Trump, as since June of this year he has been quite vocal that Powell should not raise rates.

The Feds are non-partisan and to effectively operate are independent of political interference. As customary, president’s and those in leadership refrain from making comments about monetary policy. That is most, except Trump who once again has demonstrated his lack of understanding regarding political protocol.

“I’m not thrilled,” Trump said in an interview last month

Powell has stood firm and justified the move to control a positive economy. The discount rate is the cost commercial banks pay for funds. Their impact does not immediately affect consumers but they typically result in higher borrower costs.

You can’t have it both ways

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 2 to 2-1/4 percent. Jerome Powell, Fed Chairman

Ever since the financial meltdown of 2008, systemic changes were adopted to strengthen the economy. In Trump’s case, even though it is very tough for him to admit he inherited an economy that had all the signs of positive growth, as a practical measure it must be properly managed. As the economy moves forward, it is the Fed’s who are in control of monetary policy and to manage interest rates so that inflation of other negative factors are mitigated.

The nine member panel of the Federal Reserve Open Market Committee voted unanimously to support the increase.

As expected this week’s mortgage numbers saw a slight increase of two basis points to come in at 4.54% The increase is predicated on economic data which continues to show improvement. Another key factor to support the notion that rates will continue to climb is the latest jobs report which saw new jobs at 201,000.

While rates have risen, the biggest dilemma for those who desire a new mortgage is finding homes that are within their affordability range. As an example, in a year over year comparison rates have increased nearly seventy-five basis points or three-quarters of a percent. So, while it is great the economy is moving forward, consumers must deal with the reality that cost of goods and services also increase.

The result is affordability remains a solid metric but the key with mortgage rates is timing and being in a position to qualify and take advantage of mortgage rates based on your budget.

The impact

Average Mortgage Amount – One Year Analysis

Average

Sept. 2018

Sept. 2017

Mo Diff

Nationwide

$202,000

$1,069

$939

-$130

California

$320,000

$1,642

$1,487

-$155

While the mortgage of choice remains a 30-year fixed rate based on its amortization to provide more affordable payment, the average mortgage term is approximately seven years (based on data that consumer needs of refinancing).

As mentioned rates have risen, likewise the economy has also strengthened. For most consumers it’s a dollars and cents evaluation, so in their mind the rise is rates is of concern or something that impacts their buying power. As an example, nationwide the difference of $130 each month translates into $1,560 annually or $10,920 based on a seven-year term. Specifically for those in California the numbers are $155 monthly or $1,860 annually which is $13,020 based on the seven-year term.

The question remains; can your budget handle the increase? does the touted tax-cut provide enough money back into your budget to mitigate the increase?

A snapshot of this week’s mortgage rates (popular programs)

Mortgage rates inched up this week to land at 4.520%. The one basis point rise in week over week reporting is not the biggest news. The rate represents the benchmark thirty-year conventional mortgage.

(Photo by Mannie Garcia/Bloomberg via Getty Images)(Photo by Joshua Roberts/Bloomberg via Getty Images)

Low rates do not mean a thing if you can’t find an affordable home!

Affordability index

For most homebuyers or even those wishing to take advantage of low rates, the trick is having the credit to quality and having the down payment (or sufficient equity). Recently, another element has been added to the equation of securing a home; finding an affordable property. For many the reality of an “average home price” results in sticker shock. Some parts of the country have the price well over $500,000, and that is for first-timers!

The result of would be buyers remaining on the sidelines is a reduction of mortgage applications. If the pace continues, expect lenders to trim staffing so their operations are “right-sized.”

Rates are cyclical and while many in the public policy arena tout a positive economic environment, for homebuyers that news triggers higher interest rates as well as higher home prices.

Here is a snapshot of this week’s rates:

August 30, 2018

30-Yr FRM

15-Yr FRM

5/1-Yr ARM

Average Rates

4.52 %

3.97 %

3.85 %

Fees & Points

0.5

0.5

0.3

Margin

N/A

N/A

2.77

Freddie Mac is an institutional investor and provider of mortgage funds to local lenders who work with consumers but sell the mortgages to them. Each week they publish the mortgage market rate survey which is data obtained from a sample of their pool of lenders.

[Expo Park – Los Angeles, CA] Last Thursday the California African-American Museum hosted the final symposium series on gentrification. The event was created by Karen Mack of L.A. Commons. “Evolution of View Park: Making Sense of Gentrification” featured great audience participation, some solid questions and an excellent presentation.

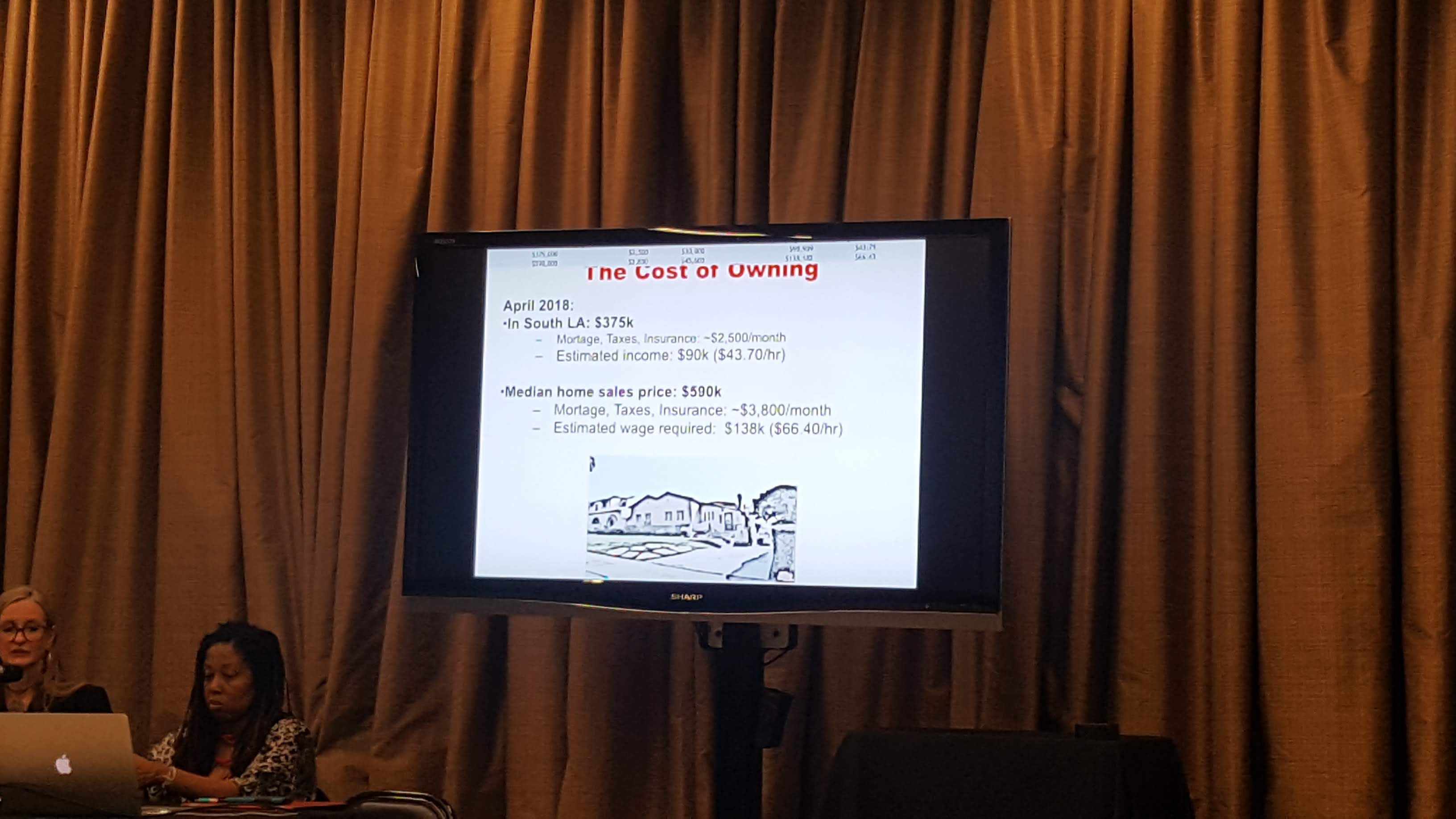

South Los Angeles is ripe for gentrification as the average home price sets at $375K

Complex topic

As mentioned in previous articles on this series; the gentrification topic is very complex and one that can be quite emotional in discussing, particularly from the brave souls in attendance who offered compelling anecdotal commentary. These types of events are eye-openers as the commentary offered by the audience oftentimes transforms into a venting session which is necessary to put the topic front and center. However, it can be precarious as the venting can go on and on…….leaving very little room for solutions based strategies to be communicated.

“This series has been so successful Karen should take it on the road” Robert Lee Johnson, Community Author

The event started at 2pm and once again the venue was packed to the brim. As predicted due to the primary area of discussion; View Park, the majority of those in attendance were African-American.

Crack epidemic in the 80’s

The civil rights movement of the 1960’s as well as the dismantling of racial covenants which previously kept African-Americans from moving into certain communities was critical as there was an increase in the movement towards achieving middle class status through home ownership.

Families grew at an impressive clip. What gets lost in the whole gentrification discussion, particularly trying to answer the question of if certain neighborhoods or property was hard to achieve why did some of those same families leave and flee to the suburbs and other areas? For those who cherish Ronald Reagan as an icon of growth while perpetuating the “American dream,” those from the African-American communities have a different perspective. It is well documented funds needed to fight the Nicaraguan war as well as other conflicts in Central and South America came from the purchase of the readily supply of cocaine. The product found haven in urban centers across America. The result was turf battles, killings and other negative consequences which dismantled neighborhoods that were once beacons of progress and hope. As those areas decayed, it became ripe for reinvestment to replace current occupants.

Legacy and affordability

A key theme or issue which many were seen nodding their heads in agreement was the notion that offspring of those who purchased property in the 60’s, 70’s, 80’s and beyond have great difficulty in being able to purchase their own home, today! While that is a statement many seem to affirm, it raises many questions. Did those parents who originally purchased home not do an adequate job in helping their offspring achieve financial literacy? Due to their successes, did they seem to project a road that their offspring would not have to work or sacrifice like they did? Why do they assume their offspring cannot qualify for financing, while admitting their incomes are perhaps higher based on the age they first purchased? It is more complex then assessing those who grew up in the area cannot afford the very area they grew up in.

Reverse racism?

The interest in the symposium topic was obvious based on packed crowds at each event. There was a strong sentiment of how homeownership was achieved and how it was critical for them to create a legacy for their heirs. More important was the need for African-Americans to maintain those neighborhoods.

United States history is ripe with laws, regulations, discrimination and other tactics to deprive groups such as African-Americans from owning property or relegating them to specific communities. Some in attendance were quick to point out their pleas to keep neighborhoods in the hand of African-American should not be construed as defining them as racist. Technically that would be impossible as racism is using race to oppress other ethnic groups. African-Americans are not creating any laws or systemic maneuvers to keep any out.

Solutions

As mentioned due to the venting there was more assessment of the problem versus solution. However, that is to be expected as what Karen Mack organized was a starting point to discuss the issue and that is crucial for stakeholders to speak to their issues.

One important theme offered by those presenting possible solutions was the need to become organized and take a more active role in legitimate organizations.

Due to time the event had to conclude but many in attendance committed to taking this discussion offline and continue to address issues to combat the negative reality of gentrification.

Readers are encouraged to educate themselves on this topic. Karen Mack may or may not agree to a road show, in the meantime those interested must stay engaged in community platforms such as the one which brought folk together for this series.

Creating some relief for those obtaining a new mortgage, rates slid down 10 basis points in week over week reporting. This morning job numbers also posted impressive gains, despite Donald Trump breaking a long-standing policy of intimating the news prior to the official release with one of his early morning tweets. The issue is the Bureau of Labor Statistics is to be the first voice in officially releasing the numbers, which normally is around 8:30AM . Period!

In Trump fashion while he did not specifically break protocol, his mere mention was enough to cause consternation for those who treasure integrity from our institutions.

These two metrics and other positive signs bode well for those in political control and could be enough to keep them in the driver’s seat. The unknown is will they be enough to fend off the impending blue wave from the November election that could result in Democrats gaining control of one or both seats of Congress?

Those in control insist the majority of voters are only concerned about kitchen-table issues and pay little attention to the other dilemmas Trump and the ruling party are attempting to deal with. They are banking on as long as impressive economic numbers are achieved, any other issues are secondary and will keep them in control.

Of course, Congressperson Maxine Waters (D-California) who has been a thorn in the side of Trump and his supporters sent out a warning while appearing on a national news program earlier this year in March.

“for if some reason, Robert Mueller does not get him, Stormy will.”

An increase of six basis points is normal within week over week reporting. However, it is the trend which has many borrowers showing signs of concern. The benchmark thirty-year mortgage crept to the highest point of 2018 and now sit as 4.610%. The news was reported yesterday as Freddie Mac released its primary market survey which tracks mortgage rate movement.

A seller’s market

Adding consternation to those in the market to purchase a home is the fact the current market is defined as a “seller’s market.” That translates into fewer properties on the market, thus buyers have been forced to make competitive offers and the result is higher sales prices.

Those in the market to purchase a new home or refinance their existing mortgage usually take a very cautious position when contemplating a transaction. The economy has been on a nine-year recovery and each month there has been improvement. Unemployment is at record lows. Some have received bonuses or extra money in their paychecks. All of this may sound good on a political front, however the increase in rates represents higher cost and puts first time buyers in jeopardy as there is added pressure on them to qualify for a loan.

Rates have increased approximately fifty basis points from a year over year comparison

Here is a snapshot of rates for popular programs:

May 17, 2018

30-Yr FRM

15-Yr FRM

5/1-Yr ARM

Average Rates

4.61 %

4.08 %

3.82 %

Fees & Points

0.4

0.4

0.3

Margin

N/A

N/A

2.77

** each week Freddie Mac publishes the rate survey. It is retrieved from a sampling from its lenders who sell mortgages to them. The report is an industry standard and used to gauge consumer mortgage rate movement.

[Exposition Park – Los Angeles, CA] This past Thursday the California African-American Museum (CAAM) hosted L.A. Commons and Mrs. Karen Mack in a community symposium titled the “Evolution of View Park.” This was the second of a three-part series focusing on “Making Sense of Gentrification,” highlighting the community of View Park (Los Angeles), CA.

Mrs. Karen Mack welcoming attendees. photo courtesy of fredyt123

A standing room crowd came out to hear and discuss what is one of the hottest topics in the past twenty years. Gentrification is not an easy topic to discuss. The word evokes emotion and for many has a negative meaning. Although from my lens those in attendance were predominately African-American, homeowners and female, for the most part there was a good degree of diversity from other ethnic groups. What also made for a good discussion was the span of age groups. In addition to the focus on View Park, some who have called the community home represented multi-generational families. You also had representation from neighboring communities such as Baldwin Hills, Leimert Park, West Adams and Venice, just to name a few. Additionally, there was representation from cities such as District of Columbia, Baltimore and other cities on the east coast. Sprinkled in the audience were a few millenniums who were courageous to share their perspectives.

Mrs. Mack brought quite a team to inform those in attendance but to also motivate dialogue which is essential in fostering honesty about the subject matter. She was joined by economist Dr. Devin Bunten who has researched the effects of gentrification throughout communities in the United States. The data he was able to cull together to add to his presentation was unapologetic as it was supported by solid documentation. This helped the audience frame a better understanding in answering the What and the Why, as well as the How of Gentrification.

View Park and neighboring Windsor Hills are just two enclaves where today African-Americans maintain over 70% occupancy. They are treasured communities due to property type and proximity.

Also, joining Mrs. Mack was local community historian Mr. Robert Lee Johnson. The grassroots work he has done was well received because he was able to dig back to the evolution of various communities and discuss how they have come to define themselves in 2018.

Lee pointed out how African-Americans migrated from the south. For housing they were relegated to Central Avenue or the “eastside.” Legal segregation was a reality. However, as legal victories were achieved in the 60’s and racial property covenants were ruled unenforceable, African-Americans were afforded housing opportunities that those before them could not enjoy. Many find it hard to believe that Compton, CA was once all white!

Those who were stacked in the Central Avenue corridor took advantage of the legal victories and moved in all directions. Some went west to West Adams, Leimert Park as well as View Park and Baldwin Hills.

The motivation

Gentrification primarily occurs in the urban core and surrounding communities. Communities such as View Park are desirable for a variety of reasons. As beautiful are these areas are, for those looking to move closer to the urban core they must contemplate life in a more multi-cultural environment versus an area they may have grown up in, such as the Westside or other bedroom communities in the suburbs.

By selecting to relocate patient buyers are rewarded with savings in the hundreds of thousands of dollars. The biggest issue they face in coming to the new community is the realty of instead of being in the majority, they find themselves in the minority. Also, part of their acceptance in relocating is understanding services they have come to accept, might be lacking in the new neighborhood, however they can be transformed. Blending those needs into their new community is one of the biggest challenges of gentrification. That is, making sure the new services are appreciated by the current residents so they don’t feel like outsiders.

After the presentations those in attendance came prepared to ask questions and provide their anecdotal realities. The discussion was very candid and became quite emotional. Some felt the current gentrifi’ers are more like invaders.

“THEY WALK THE NEIGHBORHOODS WITH THEIR DOGS AND TARGET PROPERTIES WHICH ARE VUNERABLE, PARTICULARLY WHERE SENIORS MAY BE LIVING ALONE”

“THEY COME TO THE COMMUNITY WITH A HAPPY FACE AND BRING COOKIES AS A RUSE TO DEVELOP FRIENDSHIPS BUT THE REAL MOTIVATION IS TO GET THE HOMEOWNER TO FEEL COMFORTABLE IN DISCUSSING PURCHASING THEIR HOME.”

“THEY WORK WITH LOCAL CODE ENFORCEMENT AGENCIES WHO SCOUR COMMUNITIES LOOKING FOR VARIOUS VIOLATIONS WHICH RESULT IN THE CURRENT OWNERS FEEL THEY ARE HARRASSED. OR THEY RECEIVE FINANCIAL PENALTIES WHICH JEOPARDIZE THE CURRENT OCCUPANTS ABILITY TO PAY.”

“WHILE EVERYONE WANTS A POSITIVE COMMUNITY, THOSE WHO ARE ABLE TO MOVE IN HAVE THE FINANCIAL RESOURCES AND POLITICAL VOICE TO MAKE IMPROVEMENTS THAT CURRENT OCCUPANTS MAY HAVE LACKED. CONSEQUENTLY, AS COMMUNITIES ARE ENHANCED AND DEVELOPED THE RESULT IS HIGHER TAXES WHICH THREATENED CURRENT OCCUPANTS BASED ON THEIR INABILITY TO HAVE THE INCREASE IN INCOME NEEDED TO REMAIN IN THEIR PROPERTIES.”

“THERE IS GREAT CONCERN CURRENT FAMILY’S WILL NOT BE ABLE TO SUSTAIN A LEGACY FOR THEIR CHILDREN AS BASED ON THEIR FINANCIAL PLIGHT, BATTLING RACISM AND OTHER SYSTEMIC ISSUES MAKES IT VERY HARD FOR THEM TO BE ABLE TO AFFORD THE WAY THEIR PARENTS DID.”

The majority of issues raised by the audience was well received as you could see many heads nodding in approval. At the same time, some issues were like self-inflicted wounds as some claimed to be unfairly targeted or harassed. Based on what they were representing their behavior is the type that falls prey to being targeted. Illegal add-ons or other enhancements which might have made the property more livable, in fact are out of code. The result may lead to financial penalties or decrease in value based on what they represent their properties to be. The key, and most homeowners understand this, is to make sure their property is within code or not a target from any scrutiny, let alone a gentrifier who may feel their property is a potential purchase.

The bottom line is Mrs. Mack provided an opportunity for folk to gain information, network and become more empowered. Gentrification may have a negative connotation but understanding how it works is essential so that one has a workable answer why and how groups are reclaiming parts of the city. In the meantime, while people continue to move or relocate for a variety of reasons, much of it justified, those who remain are encouraged to take a page from the 1960’s which saw one of the early migrations of folk leaving the city for what they perceived as “greener pastures.” Don’t Move! Improve!!!

A Historical Perspective:

Racism, White Flight, Gentrification

As mentioned Racism, White Flight and Gentrification are words many have a difficult time discussing.

Racism is not a new clothing line! White Flight is not a new dance step! Gentrification is not a new gelato flavor!

Racism is a by-product of white supremacy. Gentrification is the reverse of White Flight but still a by-product

Racism was most attributed to those who identify as “white” and whose ancestry is primarily European. A construct or a system was created where their race was used to dominate other races and otherwise maintain superiority over others through oppressive tactics, hence the birth of white supremacy.

“IF YOU’RE WHITE, IT’S ALRIGHT……IF YOU’RE BROWN STICK AROUND….IF YOU’RE BLACK GET BACK!!”

the original jim crow character. It became the symbol of institutionalized racism in the united states

Racism became a world phenomenon as whites used their domination to conquer many ethnic groups. The result was colonization. Over the years some may have thought racism was eliminated by groups reclaiming their cultures, however EVEN in 2018 it still festers in our overall society and is quite prevalent.

Many voting age African-Americans had accepting the notion in their lifetime a fellow African-American would never ascend to the office of President. That is why in 2008 they were happily stunned when Barack Obama was elected the 45th president. Likewise, as long as racism has been around many feel it will not be eliminated in their lifetime.

“When we discuss the word integration, what we are stating is the sharing of: Resources, Power & Responsibility” Rev. Dr., Martin Luther King, Jr.

Racism is often confused with prejudice and other biases. Disliking something or someone for whatever reason is much different from using race to oppress other groups. Most people have prejudices but not everyone is a racist. Therefore, many whites are not racist, per se. However, the legacy they inherited shows up in many forms of behavior as other groups attempt to migrate into the larger society.

In the 1940’s, 1950’s, the 1960’s and beyond another phenomenon was created which has it roots in racism. White Flight was the result of primarily African-Americans and other groups moving into areas once primarily occupied by whites. While there are many reasons why whites fled communities and neighborhoods they once proudly called home, the common denominator was their dislike or being uncomfortable sharing space with those such as African-Americans or those who were not like them. In other words, on the periphery they may have had friendly relationships with them, but living next could not be tolerated, thus they fled and established new communities, commonly known as suburbs.

A vital element of White Flight is acknowledging Whites or no group wants to be confined to neighborhoods were property values are decimated, or where there are inferior stores, shops or business opportunities, or where their children suffer the blow of an inadequate educational system. Most important feeling fearful because of the lack of basic services.

A critical element of disparity

Racism has a specific pecking order or domination over others. From economics, employment, housing, education and other factors necessary to fulfill the ideal of living, whites receive higher pay, better employment opportunities, more access to lending as well as better educational opportunities than non-whites. That pattern still exists today as while many groups appear to enjoy a positive lifestyle, typically the person who is white is in a much better economic position, much of it the result of racism or white supremacy. However, one must be careful to not assume whites do not make sacrifices in achieving a better lifestyle. They too work very hard and are dealt some of the same blows as anyone else. In our society they just do not have the burden of being considered “less-than” or other pitfalls which systematically stymies their growth.

“All things being equal if one could insure steady employment, thus steady compensation they too would be in a position to pay their debts in a timely manner resulting in stellar credit”

Gentrification

White Flight does not mean every white person left their community as soon as a non-white showed up. However, as the dominant group shifted, communities across the United States, particularly those in major cities or those known as large urban Cities started a slow process of deterioration. As whites left, they rightfully took their resources, especially in the form of a thriving tax base.

Compounded with the reality of a disparate economic condition, non-whites simply had an inferior economic standard based on the pecking order of racism and discrimination, so living standards were directly compromised.

Those urban areas once occupied by whites were always technically called ghettos. However, the connotation drastically changed once non-whites claimed the space. As resources necessary to maintain those areas took on a slow stream of deprivation, the result was the creation of blight and other negative consequences as well as social forces such as crime and a variety of factors which rendered those areas unattractive.

Gentrification is a subtle, yet specific process. Communities which were defined as deplorable are stimulated with resources as they are redefined. People who are part of the reclamation are for the most part white, and interestingly the off-spring of the very families who fled during White Flight. Through the systemic reality of racism, they are in a better economic and educational position than those who will greet them as neighbors. Thus, rebuilding the communities becomes strategic and transformational. So instead of day-to-day survival, due to their economic standing they are able to execute a more sustainable lifestyle.

The core reality of gentrification is many who remain in those areas which are being reclaimed or who have paltry resources eventually are dealt the blow of being dislocated. This is created from the basic notion of being priced out due to higher taxes or not fully comprehending the windfall they might receive for their property is never enough, thus communities are broken up; literally one house, one block at a time until it is transformed into an oasis for the current occupants.

The news is not enough to create panic but mortgage rates reached their highest level of 2018 and now sit at 4.470%. That is the rate reported by Freddie Mac from their weekly primary market rate survey, which is the industry standard for gauging consumer mortgages. It represents the benchmark thirty-year mortgage. The survey is compiled from a sampling of lenders who sell mortgages to them.

The increase represents a five-basis point increase from week over week reporting. Among other things the rate increase is attributed to the uncertainty over the impact of tariffs which the Trump administration recently announced.

Most consumers understand mortgage rates are cyclical and even the five-point increase would be considered normal movement. On the other hand, those in the market for a mortgage pay attention to trends as positioning is a big factor in determining when to apply for a loan. Purchase transactions are driven by the close of escrow and refinance transactions take approximately sixty days to close. So, if the assumption is that rates will further increase it is more prudent to lock in the rate at time of application. Of course, if your analysis conclude rates might drop, then your strategy might be to submit your application but “float” the rate or lock in at a later time.

Tax Cuts

The financial projection for 2018 was that rates would increase from their 2017 level. There was much fanfare about the historic tax bill which was passed in December 2017. Hopefully you were lucky enough to receive bonuses touted by the majority political party as well as Donald Trump?

“Still, the vast majority of adults don’t seem to have sensed the effects of the tax cut on their personal finances.” Politico

Although the public still hasn’t been told of how the government plans to pay for the tax cuts which by 2020 will push the tax deficit pass the TRILLION-dollar mark, many have taken the position to support anything which puts a little money in their pocket, even on a temporary basis.

Donald Trump proclaims tax cuts will revolutionize economy. Some are still waiting on promised bonuses or larger paychecks.

Expect Mark Short to be taken to the woodshed

Perhaps he misspoke but later this week do not be surprised if Trump and his strong allies do not take one of their own directly to the woodshed. Why? There was so much hype in attempting the justify the tax cuts and/or more money in worker’s paychecks, one would surely assume the numbers would be more than five percent!!!!

However, contrary to what the Trump administration has been boasting their own Director of Legislative Affairs and Assistant to the President for U.S. President Donald J. Trump, Mark Short belted out on “Meet the Press” that there is good news as five million people have financially benefited from the tax bill passed in December. The problem with Short’s assessment is while five million represents lots of folk, it represents less than five percent of the total workforce which is nearly 125 million, as reported by the Bureau of Labor Statistics. Wasn’t it presented that nearly every worker would see an immediate gain? Maybe you were one of the lucky five million?

Hear Short’s specific comment at the 40 second mark.

Cost of good increase

Everyone appreciates a good economy. The result is consumer confidence has increased and that is a positive sign which doesn’t get much debate.. The impact for most consumers is even though they have more money in their pocket, the increased cost of goods has eaten away at those gains.

People take part in a protest against the Republican tax bill in Los Angeles, California on December 4, 2017. Democrats and many economists warn that the GOP tax plan gives large tax cuts to corporations and the wealthy and will hurt middle class families. (Photo by Ronen Tivony/NurPhoto)

On the mortgage front today’s rate represents a fifty-basis point increase from year over year reporting. The result is the average consumer ($244,000) is paying an additional $102 per month over a tad over $1,200 for the year. Based on those numbers you will need more than a tax cut or bonus to break even.

You’ve seen the character who professes everything he touches turns to gold? Or, they profess being truly self-made while convincing themselves and those who fall prey to their hustle they possess the magic to make lives better?

In the example of Donald Trump, he has convinced those who believe him that anything and everything President Barack Obama accomplished, in fact had a negative impact to their lives. Worse, he has convinced them any success they currently have or that they project to have is the direct result of him taking over as the 45th president of the United States.

Hundreds of thousands have already started the pilgrimage to Memphis, TN. Millions more are expected to join those for local activities or tune in to participate on Wednesday, April 4th in the commemoration of the 50th anniversary of the assassination of Rev., Dr. Martin Luther King, Jr.

Dr. King was an influential leader who had developed exceptional oratorical skills. As Donald Trump continues to boast his prowess, including his followers or base supporters who feel he is the core reason for the success of the economy, they are unfortunately missing a basic reality! No doubt there is positive movement in the economy but what gets lost with partisanship or trained pundits who have taken a blood-oath to never make any comments which might be perceived as minimizing Trump’s achievements are the facts of what he inherited in what most agree were positive signs targeted for future growth.

One of Dr. King’s famous quotes in trying to help leaders understand the plight of negroes (African-Americans) and the negative legacy of slavery, Jim Crow and institutional racism which resulted in insuring that population would always remain deficient, was the bootstrap example.

“It’s all right to tell a man to lift himself by his own bootstraps, but it is cruel jest to say to a bootless man that he ought to lift himself by his own bootstraps.” Dr. Martin Luther King, Jr. April 1, 1968

Barack Obama made sure Trump had boots

Dr. King’s words have an interesting parallel with what Barack Obama received when he assumed the presidency versus what he left for Donald Trump.

Many have forgotten or have wiped out of their minds what was going on in 2007 and 2008. Economically, things were as bad as one could imagine and president Obama could have been defined as that “bootless man.”

Eight years later or when he handed over the reins to Donald Trump the economy had already made a recovery. There were unprecedented measures of success that even the most ardent Obama critic would have to admit. The result is yes, the economy continues to rack up impressive numbers but the notion that Donald Trump has achieved it all by himself or didn’t inherit anything positive from the Obama administration would leave a reasonable person scratching their head. Dr. King would caution Trump to be a bit humbler and remind him it is more honorable to give credit where credit is due versus proclaiming to never receiving a helping hand, especially from the lad he convinced millions that he was not a legitimate citizen. The boots president Obama left for Trump have helped improve his step.

Jerome Powell holding press conference following FOMC meeting. Generated by IJG JPEG Library. Getty Images

After approximately two months since taking over the helm as the chairman of the Federal Reserve, Jerome Powell announced a rate increase. The move was expected as while rates are cyclical they are based on a variety of economic factors. Powell and the rest of the board agreed recent unemployment numbers, household confidence and the positive direction of the economy provided justification of moving the rates one-quarter of a percent or to the highest level of the year at 1.750%.

The formal announcement via a press conference followed the Federal Open Market Committee (FOMC) meeting held earlier today. The vote was unanimous as all members of the FOMC voted to increase the rate.

“The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.” Federal Reserve.

The Federal Reserve is responsible for U. S. monetary policy and when there are positive economic signs, rate increases are a necessary buffer to control inflation or other negative impacts. During the press conference, Powell mentioned at least two more rate increases are scheduled for 2018.

The fed rate is related to what banks are charged to obtain funds.